Why David Einhorn's Bearish Argument on Assured Guaranty is Wrong

Why David Einhorn's Bearish Argument on Assured Guaranty is Wrong

This article was written on January 21st 2021. I did it on another substack and I'm just consolidating the two accounts, so as to now have a duplicate. Assured Guaranty is a company we will be writing about again, so the article is still very relevant.

On January 21st, David Einhorn released a shareholder letter outlining his short thesis on Assured Guaranty (AGO), rehashing many of the same arguments from his argument in 2017. Einhorn makes two main points. He says that AGO is not properly reserved for potential Puerto Rico losses. Einhorn says “We are short Assured Guaranty (AGO), based on our original thesis that it has several billion dollars of likely embedded losses on its exposure to Puerto Rico, where it refuses to take accounting reserves.”

His second point is that the ratings agencies are not properly implementing their own models in relation to capital adequacy for AGO. He says “After our presentation, we learned that Standard & Poor’s (S&P) was making a substantial error evaluating AGO’s international project financing portfolio. These bonds are not guaranteed by any taxing authority, yet S&P incorrectly assigns a capital charge that implies they have the safety of government guarantees. Were S&P to assign the correct capital charge, we believe it would reveal that AGO could not sustain its current credit rating. We contend that S&P is not following its own rating guidelines. We pointed this out to S&P, who essentially told us to pound sand.”

Due to the lack of success influencing S&P, Einhorn & Co., took their argument to the SEC, which regulates the Ratings Agencies. “Under Dodd-Frank, the SEC directly supervises rating agencies. So, we complained to the SEC in a detailed letter. The SEC reached out to us to let us know that the letter appeared very compelling and they would take the matter seriously. In fact, they had hired an outside advisor to help with the technical areas of our complaint. A few months later, the SEC called back to tell us they had reached a “decision point.” They had conducted an investigation by requesting information about the company’s business in an area that was not at all related to what we were complaining about. Unsurprisingly, they did not find fraud in these unrelated areas, so they would likely close the investigation. We encouraged them to actually look at the subjects we complained about. The SEC has since been silent.”

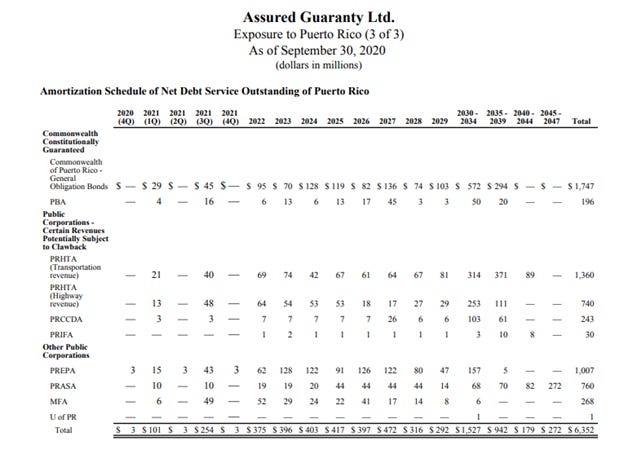

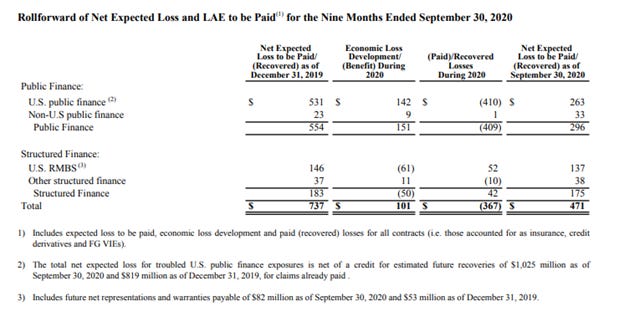

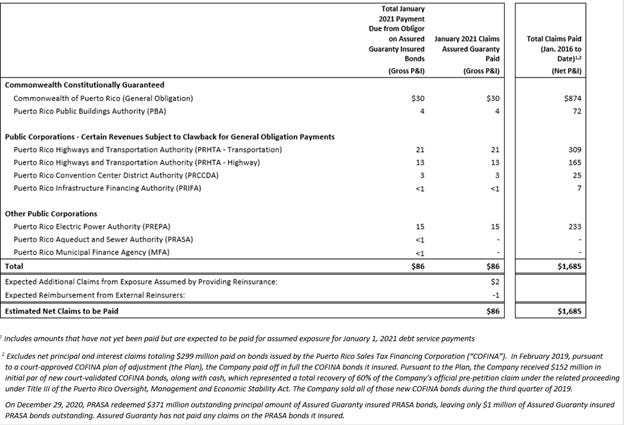

As a shareholder and long-term bull on AGO, I thought I would take a stab at addressing some of these issues. Since January of 2016, Puerto Rico has been in default on most of its debt obligations. Through January of this year, Assured Guaranty has paid out a total of $1.685 billion for its Puerto Rico obligations that are still outstanding. The Commonwealth has literally paid nothing on these obligations, despite consistently better than projected financial results and revenues. As of the end of the 3rd quarter of 2020, AGO had just under $4.1 billion in net par exposure to AGO, and $6.352 billion of net debt service. As of the same quarter, AGO had a reserve for future U.S. Public Finance losses that stood at $263MM. This is where I think some of the confusion (deception) comes in. The reserve for U.S. Public Finance losses is NET of recoveries. Historically, when municipal credits have been restructured, the recovery is a percentage of the payments missed including interest. This would mean a large cash infusion into the company that will likely cover or be close to covering any future losses with Puerto Rico.

Source: AGO 3rd Quarter 2020 Financial Presentation

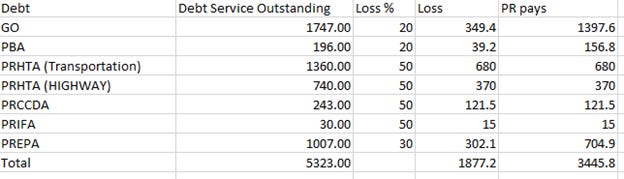

While that $263MM reserve number might have a tiny bit allocated to other credits, most of it is likely for Puerto Rico, so to make the math easier, let’s assume that it is all Puerto Rico for this exercise. Industry practices are not to disclose reserves for individual credits, as these are often contentiously litigated negotiations. PRASA and MFA have made all their debt service payments and should continue to do so based on the strength of their revenue sources, so that reduces the $6.352 billion by $1.028 billion, putting the net at $5.324 billion. Below is a table I made on the other relevant credits (omitting the $1MM for University of PR) that I think is a decent base case to work from and is not very far off from current bond prices:

Source: Tim Travis Estimates

Using these scenarios, AGO’s total loss on insured Puerto Rico debt obligations would be $1.8772 billion. Given that the company has already paid out $1.685 billion, AGO would only be on the hook for another $192.2MM, and it currently has that $263MM reserved for U.S. Public Finance. So literally, there is nearly $2 billion reserved for PR losses, but almost all future losses will be covered by the recovery. These are not overly optimistic or pessimistic projections given the quality of the credits, legal rights, and previous settlement proposals. The final number will likely be no more than a few hundred million off these estimates either way, but a very substantial cash infusion will be coming into the company. The idea that they are under-reserved for Puerto Rico by several billion dollars is simply a ludicrous statement to make. I’d also note that recent changes to the Federal Oversight Management Board have been very positive, with members showing a renewed interest in resolving the debt and allowing the Commonwealth to truly recover and grow.

Source: AGO Company Statements

Now I will spend a little less time on the 2nd claim that the ratings agencies are not properly utilizing their own capital adequacy models, which I find to be a rather weak one. The international project finance bonds that Einhorn is referencing that do not have government guarantees associated with them, are less than $17.5 billion. That is about 7.5% of the company’s $233 billion net par outstanding. The company has said that it has roughly $2.8 billion in surplus capital on its current credit ratings, which any change in methodology on those $17.5 billion in bonds outstanding are not likely to impact too severely if it did even occur. AGO has several unique entities writing insurance business, so even if the one that services international infrastructure bonds was downgraded, it would not necessarily impact the U.S.-focused entities, which write large portions of the new business anyways. It just is not some massive dealbreaker, plus more capital would be freed up, which could be used to buyback stock at dirt cheap levels, if it were ever to happen. In conclusion on Einhorn’s argument, I do not believe it to be very persuasive. I did offer to chat with him, but he did not take me up on that, which is fine, and I do respect him as an investor, but just disagree on this stock.

I will write more about AGO after the company reports 4th quarter earnings report, but the company had a 3rd quarter book value of $6.549 billion or $79.63 per share. Adjusted operating shareholders’ equity and adjusted book value were $6.07 billion and $8.885 billion, respectively. The per share numbers were $73.80 and $108.02, respectively. The stock trades at a meager $36.27, or 49% of operating shareholders’ equity and 33.57% of adjusted book value. These are some of the lowest valuation metrics in its history, yet the business is in good shape. The company has earned $2.28 per share year-to-date despite the impact of C-19, and new business production has picked up nicely, with the company already generating $264MM in PVP, up from a little over $180MM at the same time last year. The riskier and more capital-intensive U.S. Structured Finance insured par outstanding has declined from $142.2 billion in September of 2009, to only $8.6 billion. Total insured par outstanding has declined from $646.9 6 billion in September of 2009, to only $233.1 billion as of the 3rd quarter of 2020. Claims-paying resources, however, have only declined from $12.8 billion to $11.1 billion, so all the insured leverage ratios have improved. AGO has been a solid book value per share compounder via its combination of consistent profitability and accretive stock buybacks done at substantial discounts to book value. Below investment grade exposure at the end of the 3rd quarter was just under $8 billion, which is the lowest since the Financial Crisis for the company, and most of that $8 billion is related to Puerto Rico, which we discussed in detail.

Source: AGO 3rd Quarter Earnings Presentation

Certainly Covid-19 has pressured municipal finances, but actual financial results have been better than expectations for most states. The election of Joe Biden and a Democrat congress makes it extremely likely we will see even bigger fiscal stimulus, including exceptionally large financial relief to the states. 2020 is expected to be a good year for the economy as we see continued reopening and pent-up demand, combined with stimulus. AGO is in good shape and I believe the stock is a fantastic opportunity in a very overvalued market. I do not see any reason why it should not trade in excess of $55 per share, which would still be a considerable discount to book value, reflecting the currently lower return on equity the company is generating. Future earnings and accretive stock buybacks should allow the company to keep growing these metrics, while higher interest rates would ultimately be greatly beneficial for earnings and returns on equity.